In today’s fast-paced world, where financial landscapes are continually shifting, the ability to effectively balance short-term and long-term financial goals is a crucial skill for anyone aiming to achieve financial stability and success. Whether you’re saving for a dream vacation, paying off student loans, or planning for a comfortable retirement, understanding how to allocate your resources wisely can make all the difference. This article will guide you through practical strategies to harmonize your immediate financial needs with your future aspirations, ensuring that each decision you make today contributes to a secure and prosperous tomorrow. With the right approach, you can confidently navigate the complexities of financial planning, maximizing your potential for both present enjoyment and future security.

Setting Priorities for Financial Success

To achieve financial success, it’s crucial to set clear priorities that align with both your immediate needs and future aspirations. Start by identifying your short-term goals, such as paying off high-interest debt, building an emergency fund, or saving for a vacation. These objectives typically require focused attention and disciplined budgeting to ensure they don’t derail your long-term plans. Consider the following steps to prioritize effectively:

- List Your Goals: Clearly define what you want to achieve in the short and long term.

- Assess Your Current Financial Situation: Understand your income, expenses, and existing savings.

- Rank by Importance and Urgency: Determine which goals need immediate attention and which can wait.

Once your short-term needs are addressed, shift your focus to long-term aspirations like retirement savings, investing in property, or funding your children’s education. Allocate a portion of your budget to these goals by leveraging tools such as retirement accounts, investment portfolios, or educational savings plans. By systematically balancing these priorities, you can ensure a stable and prosperous financial future.

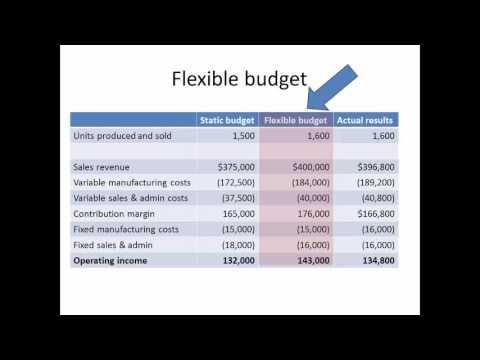

Creating a Flexible Budget for Today and Tomorrow

Crafting a budget that accommodates both immediate needs and future aspirations requires a strategic approach that aligns with your unique financial landscape. Begin by identifying your short-term necessities and long-term aspirations. Short-term goals might include everyday expenses, emergency funds, and upcoming trips, while long-term objectives could involve retirement savings, buying a home, or investing in education. By categorizing these goals, you can allocate resources more effectively.

Next, develop a flexible budget framework that adapts to life’s unpredictabilities. Consider these key strategies:

- Prioritize: Focus on urgent short-term needs without neglecting the importance of long-term savings.

- Diversify: Balance investments and savings accounts to ensure liquidity while growing your wealth.

- Review Regularly: Set monthly or quarterly check-ins to adjust your budget according to life changes and market conditions.

- Automate Savings: Use tools that automatically transfer funds to savings or investment accounts, ensuring consistent progress towards your goals.

By thoughtfully balancing your financial priorities, you can create a dynamic budget that supports both immediate fulfillment and future security.

Leveraging Investments for Long Term Growth

In the pursuit of long-term financial growth, it’s essential to harness the power of strategic investments. Diversification plays a critical role in mitigating risks while maximizing returns over time. By spreading your investments across various asset classes such as stocks, bonds, and real estate, you create a robust portfolio that can weather market fluctuations. Additionally, consider the potential of compound interest. The earlier you start investing, the more time your money has to grow exponentially. This principle is especially powerful in retirement accounts where reinvested dividends and interest can significantly enhance your wealth over the decades.

To ensure a balanced approach between short-term needs and long-term growth, prioritize the following strategies:

- Set clear objectives: Define what you want to achieve in the next 5, 10, and 20 years.

- Stay informed: Regularly review market trends and adjust your portfolio accordingly.

- Be patient: Avoid the temptation to make impulsive decisions based on short-term market volatility.

- Utilize tax-advantaged accounts: Maximize contributions to accounts like 401(k)s and IRAs to benefit from tax savings and compound growth.

By implementing these strategies, you can effectively leverage your investments to achieve sustainable long-term growth while maintaining the flexibility to meet your immediate financial goals.

Regularly Reviewing and Adjusting Your Financial Plan

To maintain a balanced approach to your financial goals, it’s crucial to consistently evaluate and modify your financial strategy. This ensures that both short-term needs and long-term aspirations are being met. A financial plan is not a static document; it should evolve with changes in your life circumstances, economic conditions, and personal priorities.

- Set Regular Checkpoints: Schedule quarterly or semi-annual reviews of your financial plan to assess progress and identify areas that need adjustment.

- Adjust for Life Changes: Major life events such as marriage, having a child, or changing careers should prompt a reevaluation of your financial goals and strategies.

- Monitor Market Trends: Stay informed about economic changes that could impact your investments and savings, and adjust your plan accordingly.

- Balance Risk and Reward: Ensure that your investment portfolio aligns with your current risk tolerance and time horizon.

By , you ensure that your financial journey remains aligned with your evolving goals and circumstances. This proactive approach empowers you to make informed decisions, adapt to changes, and keep both short-term and long-term objectives in sight.

{kind=link}