Creating a family budget is more than just a financial exercise; it’s a powerful tool that can transform your family’s future. Whether you’re saving for a dream vacation, planning for your children’s education, or building a nest egg for retirement, a well-crafted budget serves as the roadmap to achieving these financial goals. In this guide, we’ll walk you through the steps to create a family budget that not only aligns with your aspirations but also adapts to the unique dynamics of your household. With confidence and clarity, you’ll learn how to take control of your finances, prioritize your spending, and secure a stable financial foundation for your family’s future. Let’s embark on this journey together and unlock the potential of a budget that truly works for you.

Identifying Your Financial Goals and Priorities

Before diving into the nitty-gritty of crafting a family budget, it’s essential to have a clear understanding of what you’re aiming to achieve financially. Start by gathering your family and discussing your aspirations. Identify your financial goals by asking questions like: What do we want to save for? Is it a new home, a dream vacation, or college tuition? Understanding your motivations will make it easier to stick to your budget.

Next, prioritize these goals. It’s likely that not all objectives can be achieved simultaneously, so consider what’s most important to you as a family. Here’s a quick way to categorize them:

- Short-term goals: Achievements like building an emergency fund or paying off credit card debt within a year.

- Medium-term goals: Objectives such as buying a new car or saving for a home renovation over the next few years.

- Long-term goals: Plans like saving for retirement or your children’s education.

Aligning your budget with these priorities will ensure you’re channeling resources effectively and moving in the right direction. Once your goals are clear, you can tailor your budget to not only meet everyday needs but also pave the way to your financial aspirations.

Crafting a Realistic and Flexible Budget Plan

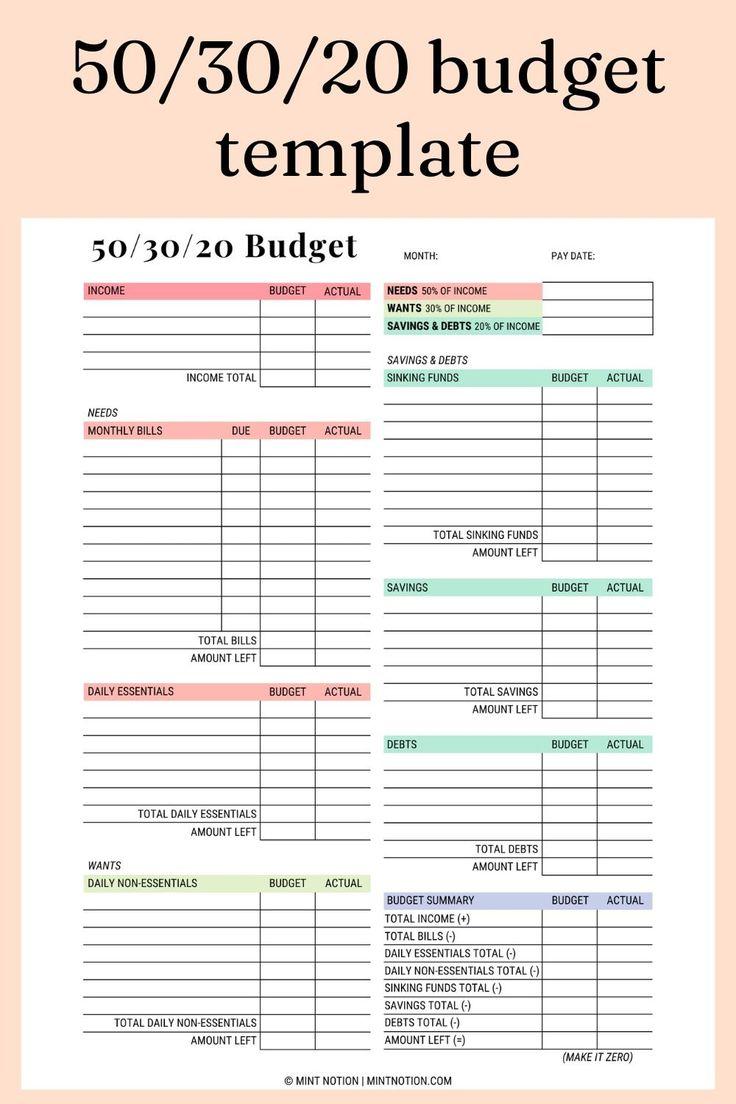

Creating a budget that is both realistic and adaptable is key to achieving your family’s financial aspirations. Start by assessing your current financial situation, identifying all income sources, and listing all necessary expenses. Fixed costs such as rent or mortgage, utilities, and insurance should be prioritized. Then, consider variable expenses like groceries, transportation, and entertainment, which offer more flexibility for adjustments. It’s essential to be honest about your spending habits to ensure your budget reflects reality.

Next, set clear financial goals and allocate funds towards them. Consider breaking them down into short-term, medium-term, and long-term categories to make them more manageable. For instance, saving for a vacation might be a short-term goal, while retirement savings represent a long-term objective. Strategies for a flexible budget include:

- Building an emergency fund to handle unexpected expenses without derailing your financial plan.

- Regularly reviewing and adjusting your budget to accommodate changes in income or expenses.

- Incorporating a buffer for miscellaneous costs to prevent overspending.

By consistently monitoring your budget and making necessary adjustments, you can create a financial roadmap that not only meets your family’s needs but also steers you towards your financial dreams with confidence.

Implementing Effective Saving Strategies

To enhance your family’s financial stability, adopting prudent saving methods is essential. Start by establishing a dedicated savings account separate from your regular checking account to avoid the temptation of dipping into your savings. Consider setting up automatic transfers from your main account to this savings account each month, ensuring a consistent contribution without having to manually intervene.

Furthermore, identifying and eliminating unnecessary expenses can significantly boost your savings potential. Analyze your monthly spending and pinpoint areas where you can cut back, such as dining out, subscription services, or impulse purchases. Instead, redirect these funds into your savings. You can also explore the following strategies:

- Emergency Fund: Aim to build a fund that covers 3-6 months of living expenses to cushion against unforeseen events.

- High-Interest Savings Accounts: Opt for accounts that offer better interest rates to maximize your savings growth.

- Discounts and Coupons: Leverage these to save on everyday purchases, allowing more room in your budget for savings.

Monitoring Progress and Adjusting Your Budget

Once you’ve set up your family budget, it’s crucial to keep an eye on your progress to ensure you’re on track to meet your financial goals. Regularly reviewing your budget allows you to identify any discrepancies between your planned and actual spending. Use tools like budgeting apps or spreadsheets to compare your monthly expenses against your budgeted amounts. This will help you understand where you may be overspending or underestimating costs. It’s also beneficial to involve your family in these reviews, fostering a sense of shared responsibility and accountability.

- Track Your Spending: Regularly update your records to reflect any changes in your income or expenses.

- Set Milestones: Break down your financial goals into smaller, manageable targets to maintain motivation.

- Be Flexible: Life can be unpredictable. Be prepared to adjust your budget to accommodate unexpected expenses or changes in your financial situation.

- Celebrate Achievements: Recognize when you reach a milestone or stay under budget for a month, reinforcing positive financial habits.

Remember, a budget is a dynamic tool that should evolve with your family’s changing needs and circumstances. By actively monitoring and adjusting your budget, you’re taking proactive steps toward achieving your financial aspirations.

{kind=link}