Creating a family financial plan is not just about budgeting and saving; it’s about crafting a roadmap that leads your family toward financial stability and prosperity. Whether you’re planning for a dream vacation, saving for your children’s education, or building a comfortable retirement fund, a well-thought-out financial plan is your compass in navigating the complexities of money management. In this article, we will guide you step-by-step through the process of developing a robust family financial plan that aligns with your goals, adapts to life’s changes, and most importantly, works for you. With confidence and clarity, you’ll learn how to assess your current financial situation, set achievable goals, and implement strategies that ensure your family’s financial well-being for years to come.

Setting Clear Financial Goals for Your Family

To establish a solid financial plan for your family, begin by identifying what truly matters. Start by gathering everyone together and discussing your shared dreams and aspirations. Are you aiming to save for a dream vacation, invest in your children’s education, or perhaps pay off your mortgage early? Clearly defined goals provide direction and motivation. Here are some steps to help you articulate these objectives:

- Prioritize Goals: Rank your financial goals in order of importance. This helps in focusing your resources effectively.

- Set Specific Targets: Define clear and quantifiable targets, such as saving a specific amount by a certain date.

- Break Down Goals: Divide larger goals into smaller, manageable milestones to track progress and celebrate achievements.

Communicate openly about these goals and ensure everyone is on the same page. This collaborative approach not only strengthens family bonds but also ensures accountability. Remember, a well-structured financial plan is a dynamic roadmap that evolves with your family’s changing needs and aspirations.

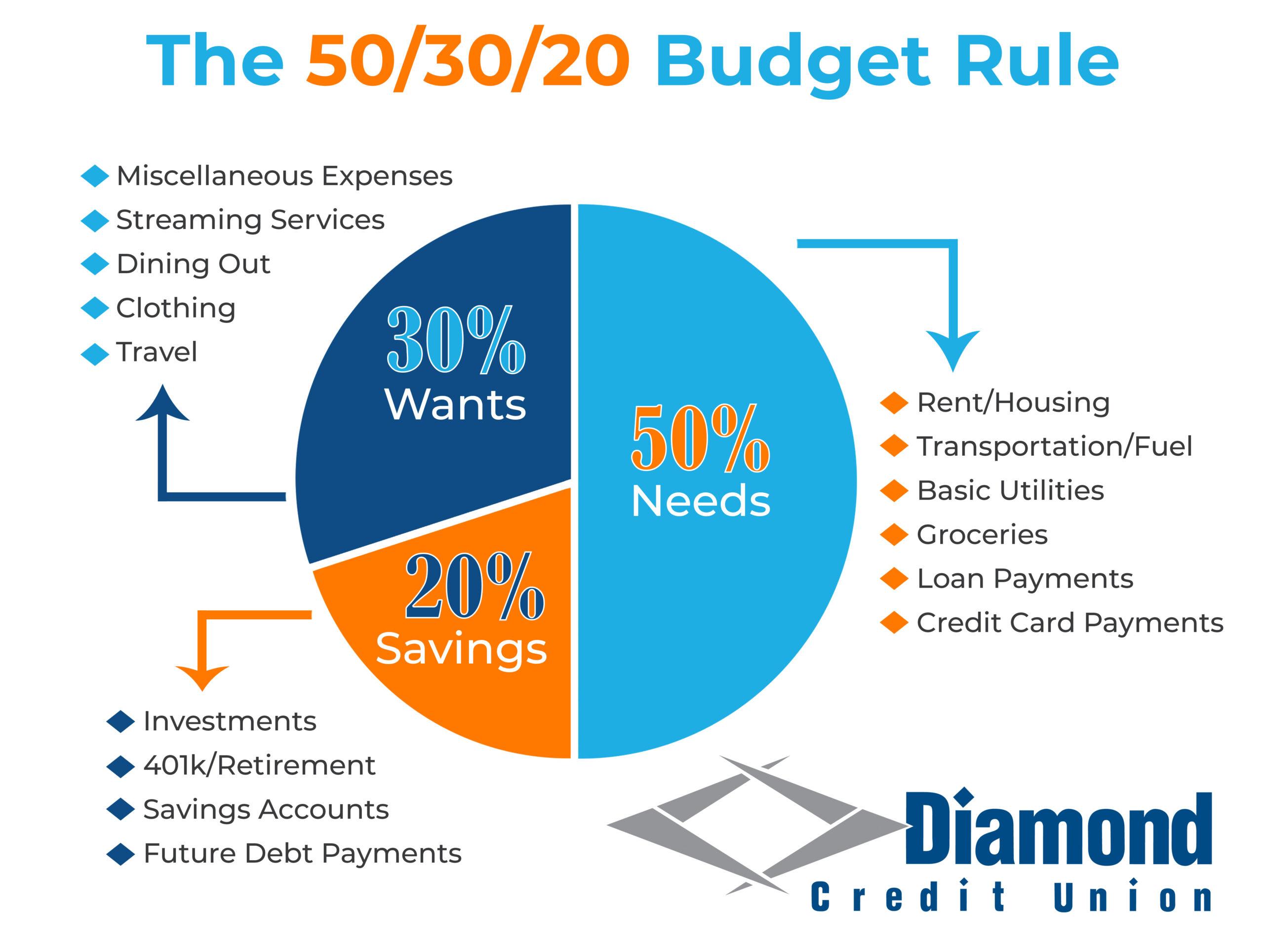

Building a Realistic and Flexible Budget

Crafting a budget that reflects both your aspirations and realities involves a delicate balance. Start by identifying your essential expenses, such as housing, utilities, groceries, and transportation. Categorize these into fixed and variable costs to understand where your money goes each month. Don’t forget to allocate funds for savings and emergency expenses, treating them as non-negotiable parts of your financial plan. This ensures that your budget is not just about managing expenses but also about building a safety net for the future.

Embrace flexibility by incorporating a buffer for unexpected costs, and revisit your budget regularly to adjust for life changes. Consider these tips to maintain a flexible budget:

- Regularly review and adjust your budget to reflect changes in income or expenses.

- Utilize budgeting apps to track spending and identify patterns.

- Set realistic goals for savings and discretionary spending.

- Communicate openly with family members about financial priorities and decisions.

Smart Saving Strategies for Every Family Member

Involving every family member in your financial plan not only fosters a sense of responsibility but also makes saving money a team effort. Here are some strategies tailored for each age group:

- For Kids: Encourage saving through a piggy bank or a simple savings account. Teach them the value of money by setting short-term goals, like saving for a toy or a book. Introduce the concept of earning through chores to help them understand the relationship between work and reward.

- For Teenagers: Open a student bank account to help them manage their allowance or part-time job earnings. Discuss the importance of budgeting and introduce them to budgeting apps. Encourage them to set aside a percentage of their earnings for future expenses, such as college or a car.

- For Adults: Focus on building an emergency fund and contributing to retirement savings. Consider automating savings to ensure consistency. Review and adjust your budget regularly to accommodate changes in income or expenses, and explore investment opportunities to grow your wealth.

- For Seniors: Prioritize healthcare and retirement savings. Review your insurance policies and adjust them as needed. Consider downsizing or relocating to reduce living expenses, and explore passive income opportunities, such as dividends or rental properties.

By adopting these strategies, each family member can play a pivotal role in achieving financial stability and success.

Implementing and Reviewing Your Financial Plan Regularly

Once you’ve crafted a comprehensive family financial plan, the journey doesn’t end there. Regular implementation and review are crucial to ensure your plan remains aligned with your family’s evolving needs and goals. Begin by setting a consistent schedule—whether quarterly or bi-annually—to evaluate your financial progress. During these sessions, assess your budget categories, track your savings growth, and measure debt reduction efforts.

- Adjust for Life Changes: Major life events such as a new job, a family addition, or an unexpected expense might necessitate recalibrating your financial strategy.

- Stay Informed: Keep abreast of economic shifts that might impact your investments or savings, and adjust accordingly.

- Celebrate Milestones: Acknowledge and celebrate financial milestones achieved, reinforcing positive financial behavior.

By maintaining a proactive approach, you not only safeguard your family’s financial well-being but also cultivate a resilient and adaptable financial strategy. Empower your family to engage in these reviews, fostering a collective commitment to financial success.

{kind=link}