In today’s world, the prospect of sending your child to college can be both an exciting and daunting financial challenge. With tuition costs steadily rising, many parents find themselves wondering how to fund their children’s education without sacrificing their hard-earned savings. The good news is that with strategic planning and a proactive approach, it’s entirely possible to prepare for this significant investment in your child’s future without compromising your own financial stability. In this guide, we’ll explore effective strategies to save for college, offering practical advice and smart solutions that will empower you to support your child’s educational dreams while keeping your financial goals on track.

Maximize Scholarships and Grants Opportunities

Securing scholarships and grants can significantly reduce the financial burden of college expenses. Begin by researching opportunities early, as many scholarships have deadlines that are months in advance. Utilize resources such as school counselors, online scholarship databases, and local community organizations to uncover potential funds. Applying for a wide range of scholarships can increase your chances, so don’t shy away from smaller or less competitive options. Additionally, ensure your application materials, such as essays and recommendation letters, are polished and tailored to each scholarship’s requirements.

Another effective strategy is to stay organized and track your applications. Create a spreadsheet to manage deadlines, submission statuses, and required documents. This will help you stay on top of opportunities and avoid missing out on potential funding. Furthermore, consider joining scholarship forums or groups where you can share tips and leads with other students. Remember, persistence is key; the more you apply, the better your chances of securing financial aid that doesn’t require repayment.

Utilize Tax-Advantaged Savings Accounts

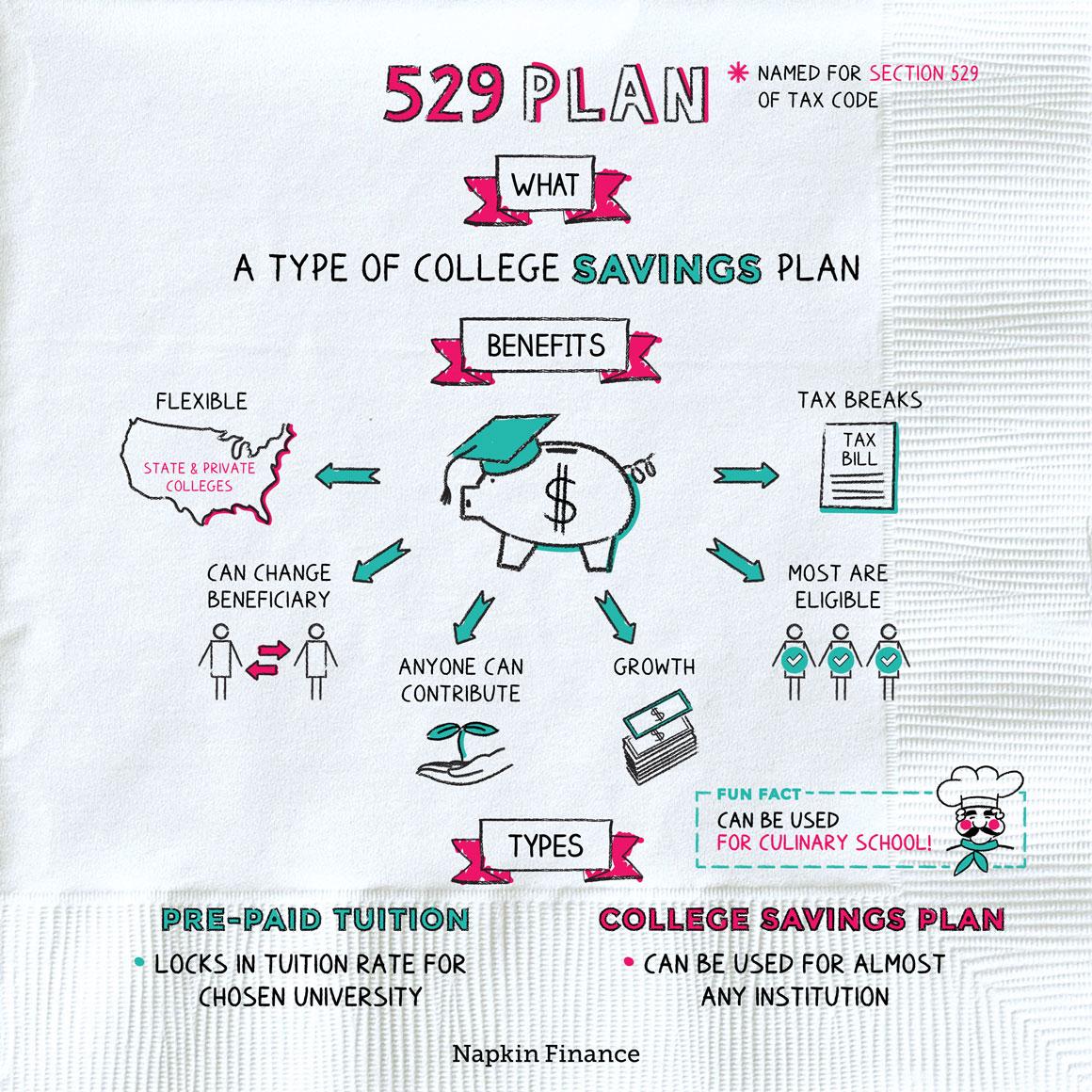

Maximize your college savings strategy by leveraging accounts designed with tax benefits in mind. 529 plans are a standout option, allowing you to grow your investment tax-free as long as the funds are used for qualified educational expenses. Contributions might also be deductible on your state taxes, offering another layer of savings. Coverdell Education Savings Accounts (ESAs) are another excellent choice, providing tax-free growth and withdrawal options for both college and K-12 expenses, though they do come with contribution limits.

When selecting the right account, consider the following:

- Contribution limits: Evaluate how much you can invest annually without penalty.

- Flexibility of funds: Some accounts offer more versatile usage, covering a range of educational expenses.

- State tax benefits: Research your state’s specific tax incentives for contributions to certain plans.

By strategically choosing and managing these accounts, you can significantly reduce the financial burden of higher education while ensuring your savings remain intact.

Explore Flexible Payment Plans and Financial Aid Options

Paying for college doesn’t have to mean emptying your bank account. Embrace flexible payment plans that many educational institutions offer, allowing you to spread the cost over manageable installments. This approach not only eases financial pressure but also helps you maintain a steady cash flow. When exploring payment plans, ensure you understand the terms, such as interest rates and fees, to avoid any surprises.

- Check if your institution offers monthly or quarterly payment options.

- Consider setting up automatic payments to avoid missing deadlines.

- Discuss with a financial advisor to tailor a plan that fits your budget.

Moreover, delve into financial aid options that can significantly offset costs. Scholarships, grants, and work-study programs are often underutilized resources that can provide substantial financial relief. Make it a priority to research and apply for these opportunities early. Leverage online platforms and school resources to discover aid tailored to your academic and extracurricular achievements.

- Apply for federal and state grants through the FAFSA application.

- Search for scholarships specific to your field of study or background.

- Explore on-campus work opportunities that offer tuition assistance.

Implement Smart Budgeting and Cost-Cutting Strategies

One of the most effective ways to prepare financially for college expenses is by embracing a smart budgeting approach. Start by analyzing your current spending habits to identify areas where you can trim excess costs. This means scrutinizing every purchase and determining if it aligns with your financial goals. Implement a zero-based budgeting system, where every dollar has a purpose, ensuring that unnecessary expenses are minimized.

Consider adopting the following cost-cutting strategies to bolster your college savings fund:

- Meal Planning: Reduce food expenses by planning meals in advance and cooking at home instead of dining out.

- Subscription Audit: Cancel unused or underutilized subscriptions and memberships.

- Energy Efficiency: Lower utility bills by using energy-efficient appliances and turning off lights when not in use.

- DIY Repairs: Handle minor home repairs yourself to save on maintenance costs.

Each small adjustment can accumulate significant savings over time, allowing you to allocate more resources towards your college fund without depleting your existing savings.

{kind=link}