As you approach the golden years of retirement, ensuring financial stability becomes paramount. With the right investment strategies, you can significantly grow your retirement fund, securing a comfortable and fulfilling future. In today’s ever-evolving financial landscape, navigating through a myriad of investment options can be daunting. However, understanding the most effective avenues for growing your retirement savings can provide clarity and confidence in your financial planning. This article will guide you through the best investment options available, offering insightful analysis and practical advice to help you make informed decisions. Whether you are a seasoned investor or just beginning to explore retirement planning, these strategies will empower you to build a robust financial foundation for the years ahead.

Diversify Your Portfolio for Long-Term Stability

Achieving a stable and growing retirement fund involves more than just picking a few stocks and hoping for the best. Diversification is a key strategy that helps mitigate risks and maximize returns over time. By spreading investments across various asset classes, you can cushion your portfolio against market volatility and increase the potential for growth. Consider incorporating a mix of the following investment options:

- Stocks: While they can be volatile, stocks offer high growth potential and can significantly boost your portfolio’s value over the long term.

- Bonds: These are generally more stable than stocks and provide a reliable income stream, making them an excellent choice for risk-averse investors.

- Real Estate: Investing in property or real estate funds can provide rental income and long-term appreciation, adding another layer of security to your retirement plan.

- Mutual Funds and ETFs: These pooled investment vehicles offer diversification within themselves, allowing you to invest in a broad array of securities without the need to pick individual stocks or bonds.

- Alternative Investments: Consider options like commodities, hedge funds, or private equity to further diversify and potentially enhance returns.

By thoughtfully combining these various investment avenues, you can create a robust portfolio that not only withstands market fluctuations but also grows steadily towards your retirement goals.

Maximize Returns with Low-Risk Bonds and Annuities

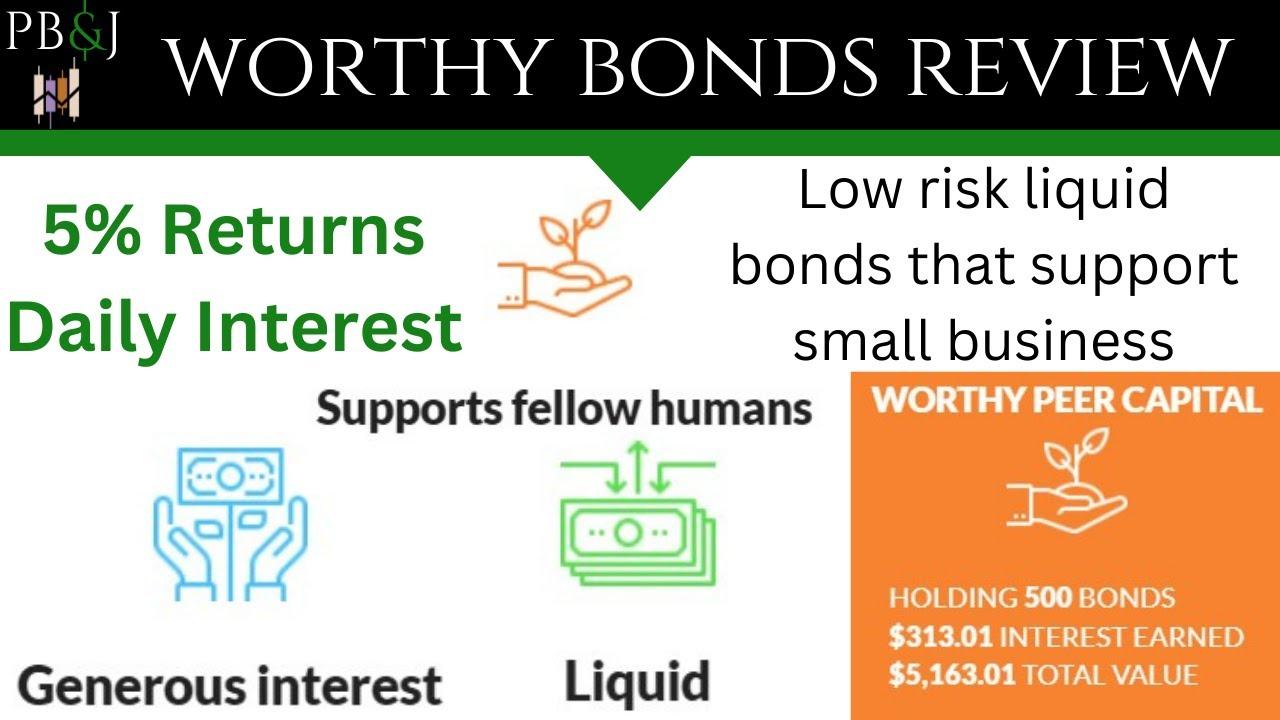

When it comes to growing your retirement fund, low-risk bonds and annuities stand out as secure and reliable options. These investment vehicles offer a way to ensure steady growth without exposing your hard-earned money to excessive volatility. Bonds, particularly government and municipal bonds, provide a predictable income stream, making them a staple for conservative investors. They function by lending your capital to a government or corporation, which in return, pays you interest over a specified period. This interest can be reinvested to compound your returns, effectively boosting your retirement savings over time.

Annuities, on the other hand, are insurance products designed to deliver a steady income during retirement. They can be customized to suit your financial needs, offering either fixed or variable payouts. Key benefits of annuities include:

- Guaranteed lifetime income, ensuring you never outlive your savings.

- Tax-deferred growth, allowing your investment to compound without immediate tax implications.

- Flexibility in terms of payout options, catering to both immediate and deferred income needs.

Incorporating these low-risk options into your portfolio can help balance more volatile investments, paving the way for a financially secure retirement.

Harness the Power of Real Estate Investment Trusts

Real Estate Investment Trusts, or REITs, offer a unique opportunity to grow your retirement fund by providing access to the real estate market without the need to directly purchase properties. With REITs, investors can enjoy the benefits of real estate ownership, such as dividend income and capital appreciation, while avoiding the complexities and high costs associated with direct property investments. By pooling resources, REITs allow you to invest in a diversified portfolio of real estate assets, including commercial properties, residential buildings, and infrastructure projects.

- Liquidity: Unlike physical properties, REITs are traded on major stock exchanges, offering higher liquidity and the ability to quickly adjust your investment portfolio.

- Income Generation: REITs are required to distribute at least 90% of their taxable income as dividends, providing a steady stream of income for retirees.

- Professional Management: With a team of experienced managers, REITs ensure that your investment is handled by professionals who maximize returns and manage risks effectively.

Incorporating REITs into your retirement strategy can provide a balance of income, growth, and diversification, making them a powerful tool for long-term financial security.

Leverage Tax-Advantaged Accounts for Greater Growth

Maximizing your retirement fund growth often involves strategic use of tax-advantaged accounts. These accounts not only provide a platform for your investments to grow but also offer tax benefits that can enhance your savings. Here are some key options to consider:

- 401(k) Plans: Many employers offer 401(k) plans with tax-deferred growth. Contributions are made pre-tax, which can lower your taxable income, and the funds grow tax-free until withdrawal.

- Roth IRAs: Unlike traditional IRAs, Roth IRAs are funded with after-tax dollars, meaning your withdrawals during retirement are tax-free. This can be a significant advantage if you expect to be in a higher tax bracket in the future.

- Health Savings Accounts (HSAs): While primarily designed for healthcare expenses, HSAs offer a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. Funds can also be invested, allowing for potential growth over time.

Leveraging these accounts wisely can lead to substantial growth in your retirement savings, offering both immediate tax benefits and long-term financial security. Aligning your investment strategy with these options can create a more robust and tax-efficient retirement portfolio.

{kind=link}