Creating a long-term savings plan for your family’s future is one of the most empowering steps you can take toward financial security and peace of mind. In today’s ever-changing economic landscape, having a well-thought-out savings strategy is not just a luxury—it’s a necessity. Whether you’re planning for your children’s education, a comfortable retirement, or unexpected life events, establishing a robust savings plan can ensure that you and your loved ones are prepared for whatever the future holds. In this article, we will guide you through the essential steps to design a savings plan tailored to your family’s unique needs and goals. With the right approach, you can build a financial safety net that will provide stability and opportunities for generations to come. Let’s dive into the practical strategies and expert insights that will set you on the path to financial success.

Establish Clear Financial Goals for Your Family

Setting a clear financial direction for your family is pivotal in ensuring a secure future. Start by identifying what you want to achieve financially, and break it down into manageable, realistic objectives. Consider discussing with your family to ensure everyone is on the same page. Key areas to focus on include:

- Emergency Fund: Aim to have three to six months’ worth of living expenses saved.

- Education Savings: Plan for your children’s education by considering 529 plans or other education savings accounts.

- Retirement Planning: Determine how much you need to retire comfortably and explore retirement accounts like 401(k)s or IRAs.

- Debt Reduction: Prioritize paying off high-interest debt to free up more funds for savings.

Regularly review and adjust these goals as your family’s needs and circumstances change. This proactive approach not only fosters financial security but also instills a sense of responsibility and foresight within the family unit.

Identify and Prioritize Essential Savings Categories

When developing a robust long-term savings plan, it’s crucial to pinpoint and rank the categories that will have the most significant impact on your family’s future. Start by evaluating your current financial situation and determining which areas are essential for your family’s growth and stability. Consider the following key categories:

- Emergency Fund: Establish a safety net that covers 3-6 months of living expenses. This fund should be easily accessible and act as a financial buffer against unforeseen circumstances.

- Retirement Savings: Prioritize contributions to retirement accounts, such as 401(k)s or IRAs, ensuring that you’re taking full advantage of any employer matches and maximizing tax benefits.

- Education Fund: If you have children, consider setting aside funds for their education. Utilize tax-advantaged accounts like 529 plans to grow savings efficiently over time.

- Debt Repayment: High-interest debts can hinder your savings goals. Strategically pay down debts, focusing on those with the highest interest rates first.

- Home Ownership: Whether saving for a down payment or paying off a mortgage, prioritize housing-related savings to build equity and reduce future financial burdens.

Once you’ve identified these categories, prioritize them based on your family’s unique needs and goals. Remember, the importance of each category can shift over time, so regularly reassess and adjust your priorities to ensure your savings strategy remains aligned with your family’s evolving future.

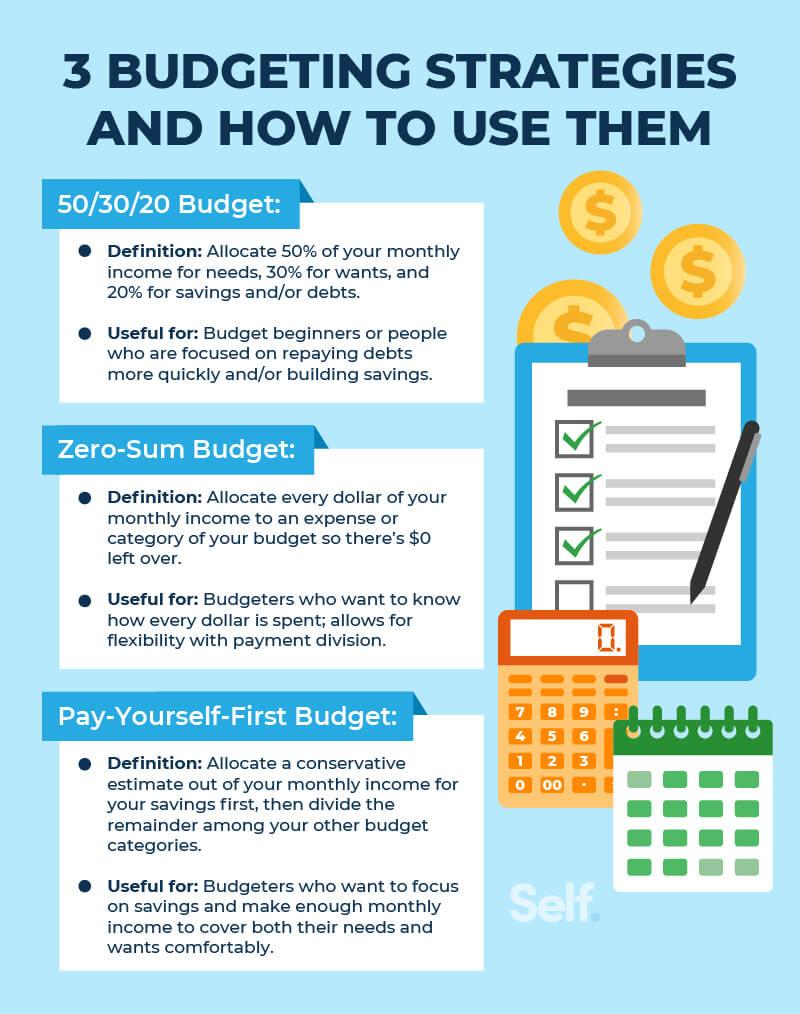

Develop a Realistic and Flexible Budget Plan

Crafting a budget that is both realistic and adaptable is key to ensuring your family’s financial stability. Start by evaluating your current financial situation, including all sources of income and necessary expenses. Identify your spending patterns and pinpoint areas where you can cut back without sacrificing your quality of life. This might involve reducing discretionary spending or finding more cost-effective alternatives for certain services.

- Set Clear Priorities: Determine what is most important for your family’s financial goals, such as paying off debt, saving for a home, or funding education.

- Include a Safety Net: Allocate a portion of your budget to an emergency fund to cover unexpected expenses.

- Adjust Regularly: Review and adjust your budget monthly to accommodate changes in income or expenses.

By maintaining flexibility, you can adapt to life’s inevitable changes while staying on track with your long-term savings plan. Remember, a well-structured budget is not set in stone but evolves with your family’s needs and goals.

Implement Effective Savings Strategies and Tools

To secure your family’s financial future, it’s crucial to adopt effective savings strategies and leverage the right tools. Start by setting clear and realistic goals for your savings journey. This might include a mix of short-term objectives, like building an emergency fund, and long-term ambitions, such as saving for retirement or your children’s education. Once your goals are defined, choose savings vehicles that align with your timeline and risk tolerance. Consider options such as high-yield savings accounts, certificates of deposit (CDs), or even investment accounts for longer-term growth potential.

- Automate Your Savings: Set up automatic transfers to your savings accounts to ensure consistency and remove the temptation to spend.

- Track Your Progress: Regularly review your savings to ensure you’re on track. Use apps or budgeting software to monitor your financial health.

- Take Advantage of Technology: Utilize tools like financial calculators or apps that help you visualize your savings goals and adjust your plan as needed.

By integrating these strategies into your financial routine, you create a disciplined approach to saving that can yield significant benefits over time. Remember, the key to a successful savings plan is not just how much you save, but how consistently you stick to your plan.

{kind=link}