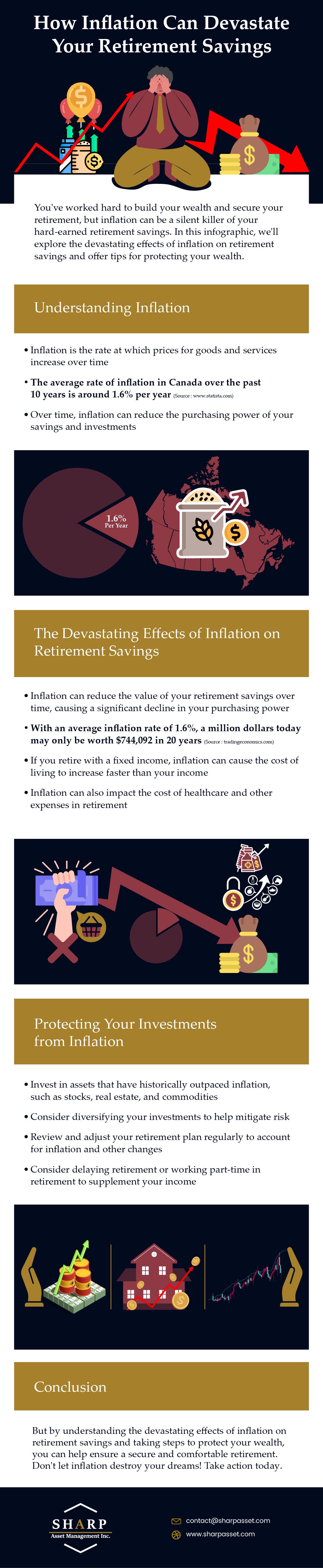

Inflation, often described as the silent thief of savings, plays a pivotal role in shaping the financial landscapes of retirees. As the cost of living gradually rises, the purchasing power of a fixed income diminishes, presenting a significant challenge for those relying on their nest egg to sustain a comfortable retirement. is crucial for anyone looking to secure their financial future. This article aims to demystify the intricate relationship between inflation and retirement planning, offering clear insights and strategic approaches to safeguard your savings against the eroding effects of rising prices. With a confident grasp of these concepts, you’ll be better equipped to make informed decisions that protect your wealth and ensure long-term financial stability in your golden years.

Analyzing Inflations Erosion of Retirement Nest Eggs

As inflation subtly eats away at the purchasing power of money, it becomes an invisible threat to retirement savings. When planning for retirement, it’s crucial to understand how inflation can significantly impact the value of your nest egg over time. Inflation can erode the real value of your savings, meaning that the same amount of money will buy fewer goods and services in the future. This reduction in purchasing power can be detrimental, especially during retirement when fixed incomes are common.

To mitigate these effects, consider the following strategies:

- Invest in inflation-protected securities: Options like Treasury Inflation-Protected Securities (TIPS) can help safeguard your savings against inflation.

- Diversify your portfolio: Including a mix of assets such as stocks, bonds, and real estate can provide a hedge against inflation.

- Consider cost-of-living adjustments: When planning your retirement income, factor in potential increases in living costs to maintain your standard of living.

- Regularly review and adjust your plan: Keep an eye on inflation trends and adjust your investment strategy accordingly to ensure your savings keep pace with inflation.

By being proactive and implementing these strategies, you can protect your retirement savings from the erosive effects of inflation, ensuring a more secure and comfortable retirement.

Strategies to Safeguard Your Savings Against Inflation

As the value of money erodes over time due to inflation, it becomes essential to adopt strategies that can help preserve the purchasing power of your savings. Here are some effective approaches to consider:

- Diversify Investments: By spreading your investments across various asset classes such as stocks, bonds, real estate, and commodities, you can reduce risk and potentially increase returns. Diversification can cushion your savings from the adverse effects of inflation.

- Invest in Inflation-Protected Securities: Consider allocating a portion of your portfolio to Treasury Inflation-Protected Securities (TIPS) or similar investments that are specifically designed to protect against inflation. These securities adjust their value in line with inflation rates, providing a safeguard for your savings.

- Real Estate and Tangible Assets: Real estate investments can offer a hedge against inflation as property values and rental income often rise with inflation. Similarly, investing in tangible assets like gold or other precious metals can preserve value during inflationary periods.

- Review and Adjust Regularly: Periodically reviewing and adjusting your investment portfolio ensures that your savings strategy remains aligned with current economic conditions and inflationary trends. Staying proactive helps in maintaining the real value of your savings.

Optimizing Investment Portfolios for Inflation Resilience

When it comes to safeguarding your retirement savings against the eroding power of inflation, strategic adjustments to your investment portfolio are crucial. Consider diversifying your assets to include investments that historically perform well during inflationary periods. These may include:

- Inflation-Protected Securities: Consider adding Treasury Inflation-Protected Securities (TIPS) to your portfolio. These government bonds are designed to increase in value as inflation rises, providing a reliable hedge.

- Real Assets: Real estate and commodities often retain their value during inflationary times. Real Estate Investment Trusts (REITs) and commodity-focused funds can be effective options to explore.

- Equities: While stock markets can be volatile, equities in sectors such as technology and consumer goods often have the potential to outpace inflation over the long term.

Moreover, maintaining a global perspective can further enhance your portfolio’s resilience. By investing in international markets, you can capitalize on regions with varying inflation dynamics, potentially offsetting domestic inflationary pressures. Regularly reviewing and rebalancing your portfolio ensures that it remains aligned with both your financial goals and the evolving economic landscape.

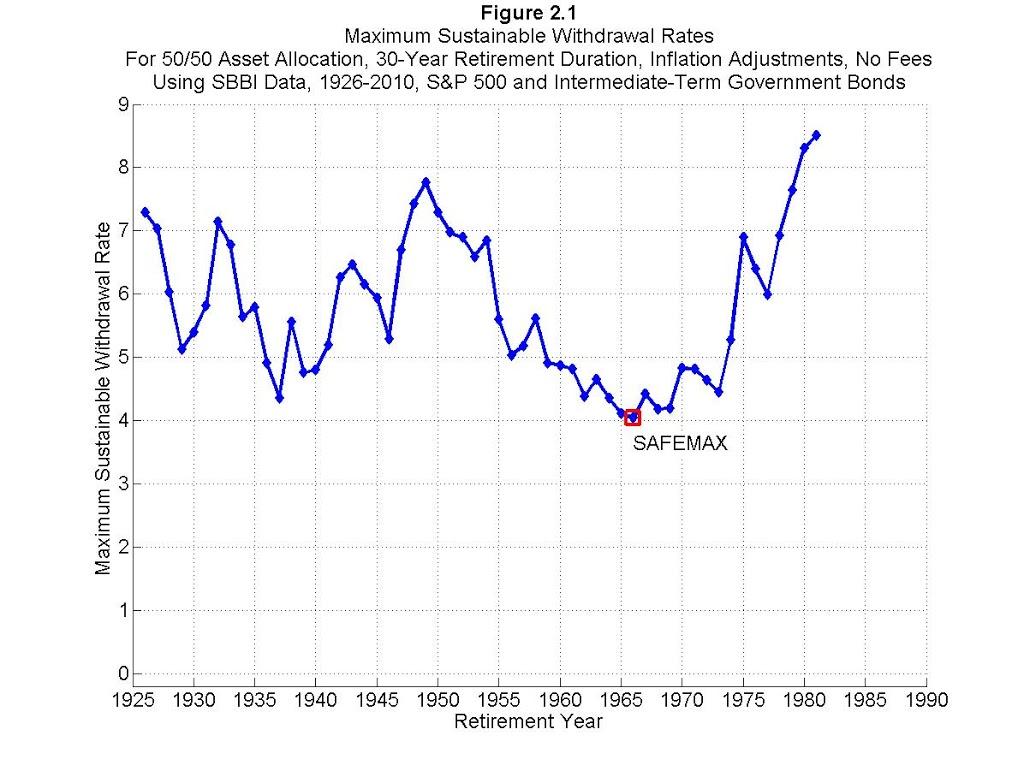

Implementing Inflation-Adjusted Withdrawal Plans

Creating a sustainable retirement strategy that accounts for inflation is crucial to maintaining your purchasing power over the years. One effective approach is to implement a withdrawal plan that adjusts for inflation. This method allows retirees to adapt their annual withdrawals based on inflation rates, ensuring their lifestyle isn’t compromised by rising costs. The key to success lies in careful planning and regular adjustments. By setting an initial withdrawal rate, often around 4%, and increasing it annually in line with the inflation rate, retirees can safeguard their nest egg against the eroding effects of inflation.

Consider these essential elements when developing an inflation-adjusted withdrawal plan:

- Track Inflation Rates: Regularly monitor the Consumer Price Index (CPI) to understand how inflation is impacting your purchasing power.

- Flexibility: Be prepared to adjust your withdrawal amounts annually to reflect changes in inflation, ensuring your spending power remains consistent.

- Portfolio Diversification: Maintain a well-diversified investment portfolio to mitigate risks and support your withdrawal needs even as inflation fluctuates.

- Consult Financial Experts: Seek advice from financial planners who can help tailor your strategy to meet your unique needs and goals.

By incorporating these strategies, you can confidently navigate the challenges posed by inflation, maintaining a stable and secure financial future throughout your retirement.

{kind=link}