Debt can feel like a heavy burden, casting a shadow over your financial future and peace of mind. Yet, there’s a strategic approach that can help you regain control and eliminate debt with confidence: the Snowball Method. This powerful debt reduction strategy focuses on paying off your smallest debts first, gradually building momentum as you tackle larger balances. By channeling your efforts into achievable milestones, the Snowball Method not only simplifies the debt repayment process but also boosts your motivation and financial discipline. In this article, we’ll guide you through the step-by-step process of implementing the Snowball Method, empowering you to clear your debts systematically and reclaim your financial freedom.

Understanding the Snowball Method for Debt Elimination

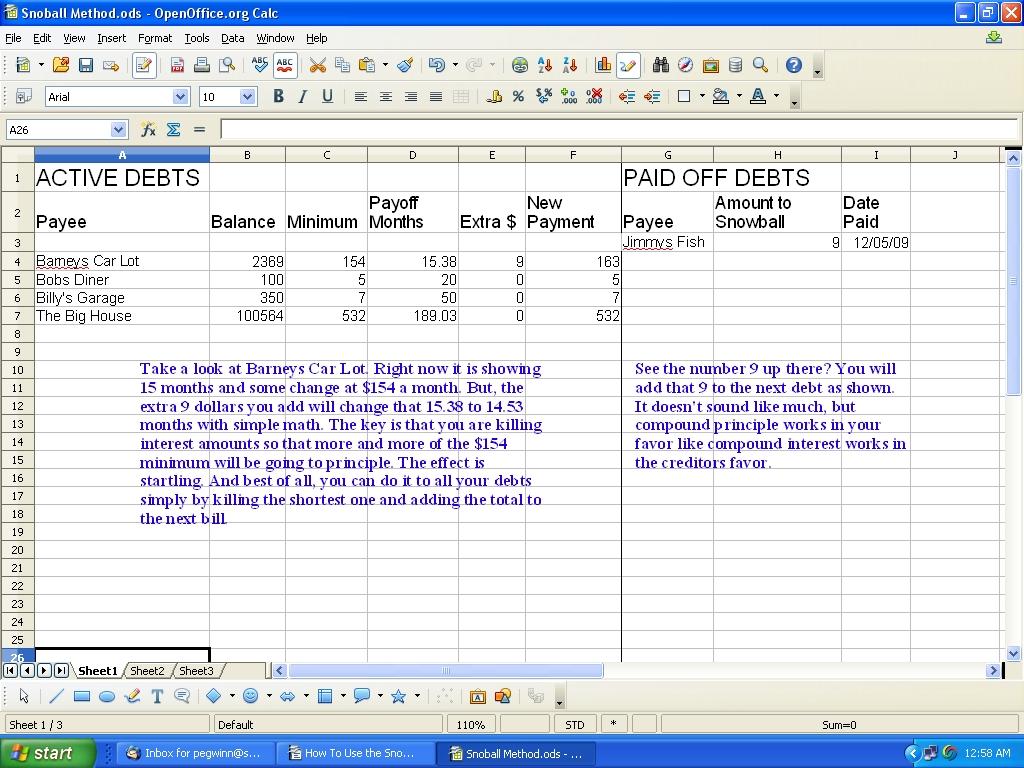

The snowball method is a powerful strategy for tackling debt by focusing on small victories that lead to larger successes. The idea is simple: list all your debts in order from the smallest balance to the largest. By concentrating on paying off the smallest debts first, you gain momentum and build confidence, turning the daunting task of debt elimination into a series of manageable steps. This approach leverages the psychological boost of quick wins, keeping you motivated to continue the journey.

Here’s how to effectively implement this method:

- List Your Debts: Write down all your debts, including credit cards, loans, and any other liabilities. Arrange them from the smallest to the largest balance.

- Make Minimum Payments: Ensure you make the minimum payment on all debts to avoid penalties and additional interest.

- Focus on the Smallest Debt: Allocate any extra funds to the smallest debt until it is paid off. This could be money saved from cutting expenses or additional income.

- Celebrate the Wins: Once the smallest debt is cleared, celebrate your achievement. This step is crucial for maintaining momentum.

- Move to the Next Debt: Redirect the amount you were paying on the cleared debt to the next smallest debt, creating a ‘snowball’ effect as you continue this process.

With dedication and persistence, the snowball method can transform the overwhelming burden of debt into a series of achievable goals, ultimately leading to financial freedom.

Prioritizing Debts for Maximum Impact

When tackling debt, understanding which obligations to focus on first can significantly enhance your financial journey. The Snowball Method is a strategic approach where you start by paying off your smallest debts first, gradually moving to larger ones. This method not only simplifies the repayment process but also boosts your motivation as you see debts disappearing one by one. Here’s how you can prioritize your debts effectively:

- List all your debts: Include every debt you owe, such as credit cards, personal loans, and any outstanding bills.

- Order them by amount: Arrange your debts from smallest to largest, regardless of interest rates. This structure helps maintain clarity and focus.

- Make minimum payments on all debts except the smallest: Allocate any extra funds towards the smallest debt until it’s fully paid off.

- Repeat the process: Once the smallest debt is cleared, move to the next on your list. Apply the same strategy, using the momentum from previous successes.

By focusing on quick wins, the Snowball Method empowers you to build confidence and maintain enthusiasm throughout your debt repayment journey. This disciplined approach not only simplifies your financial strategy but also creates a ripple effect, encouraging more substantial financial growth over time.

Crafting a Personalized Snowball Payment Plan

Creating a tailored payment plan using the snowball method involves a few strategic steps. First, list all your debts from smallest to largest, regardless of interest rate. The psychological boost from quickly paying off the smallest debt can be incredibly motivating. Focus on paying the minimum on all debts except the smallest one. Direct any extra funds toward this smallest debt until it’s paid off.

- List Debts: Order them from smallest to largest balance.

- Budget Wisely: Allocate any surplus funds to the smallest debt.

- Track Progress: Celebrate small victories to maintain momentum.

Once the smallest debt is eliminated, roll the amount you were paying on it into the next smallest debt. This creates a snowball effect, increasing your payment power as each debt is cleared. Adjust your plan as needed, ensuring it aligns with your financial goals and lifestyle. Consistency and discipline are key, and the satisfaction of watching your debts disappear will fuel your determination.

Staying Motivated and Tracking Your Progress

When it comes to maintaining your drive and measuring your achievements, the Snowball Method offers a unique psychological advantage. Celebrating small wins can significantly boost your motivation. As you knock out your smallest debts, take a moment to relish in that victory. This sense of accomplishment fuels your determination to tackle the next balance, creating a momentum that propels you forward.

To effectively track your progress, consider implementing the following strategies:

- Visualize Your Journey: Create a debt payoff chart. Each time you eliminate a debt, fill in a portion of the chart to see your progress visually.

- Set Milestones: Break down your overall goal into smaller, manageable milestones. Celebrate when you hit each one, reinforcing your commitment.

- Regular Check-Ins: Schedule weekly or monthly reviews of your debt status. This practice helps you stay focused and adjust your strategy if needed.

By leveraging these tactics, you’ll keep your motivation high and your debt repayment on track, transforming what once seemed like a daunting task into a series of achievable goals.

{kind=link}