Achieving your family’s financial milestones requires more than just good intentions; it demands a strategic approach tailored to your unique goals and circumstances. Whether you’re saving for your children’s education, planning for a dream vacation, or building a robust retirement fund, having a clear and actionable plan is essential. In this guide, we will explore the best strategies to not only reach but surpass your family’s financial objectives. With expert advice and practical tips, you’ll gain the confidence and knowledge needed to navigate the complexities of financial planning, ensuring a secure and prosperous future for your loved ones. Let’s embark on this journey to financial success together, armed with the right tools and insights to make your dreams a reality.

Setting Clear Financial Goals for Your Family

Setting financial goals for your family is crucial in creating a secure and prosperous future. Begin by envisioning what you want to achieve as a family. This could include buying a home, saving for your children’s education, or planning a memorable family vacation. Once you’ve identified these objectives, it’s important to prioritize them. Some goals might be long-term, such as retirement savings, while others could be short-term, like purchasing a new family vehicle. By distinguishing between immediate needs and future aspirations, you can allocate resources more effectively.

- Define Clear Objectives: Specify what each goal entails and the steps required to achieve it. A vague goal like “save money” becomes actionable when you specify “save $20,000 for a new car in two years.”

- Set Realistic Timeframes: Assign a timeline to each goal, ensuring it’s achievable. This helps in maintaining focus and motivation.

- Monitor Progress: Regularly review your goals and adjust your plans as necessary. This keeps the family aligned and committed to the objectives.

- Celebrate Milestones: Acknowledge and celebrate each milestone you reach. This not only boosts morale but also strengthens family bonds.

By following these strategies, your family can effectively work towards achieving its financial milestones, ensuring a stable and fulfilling future for all members.

Crafting a Realistic Budget to Support Your Milestones

Creating a budget that aligns with your family’s financial goals is an essential step towards achieving your milestones. Start by clearly identifying your financial objectives, whether it’s saving for a home, a child’s education, or a family vacation. Once your goals are set, categorize your expenses into fixed, variable, and periodic costs. This will help you understand where your money is going and identify areas where you can cut back. Fixed expenses include mortgage or rent, utilities, and insurance. Variable expenses cover groceries, dining out, and entertainment, while periodic expenses might involve annual subscriptions or car maintenance.

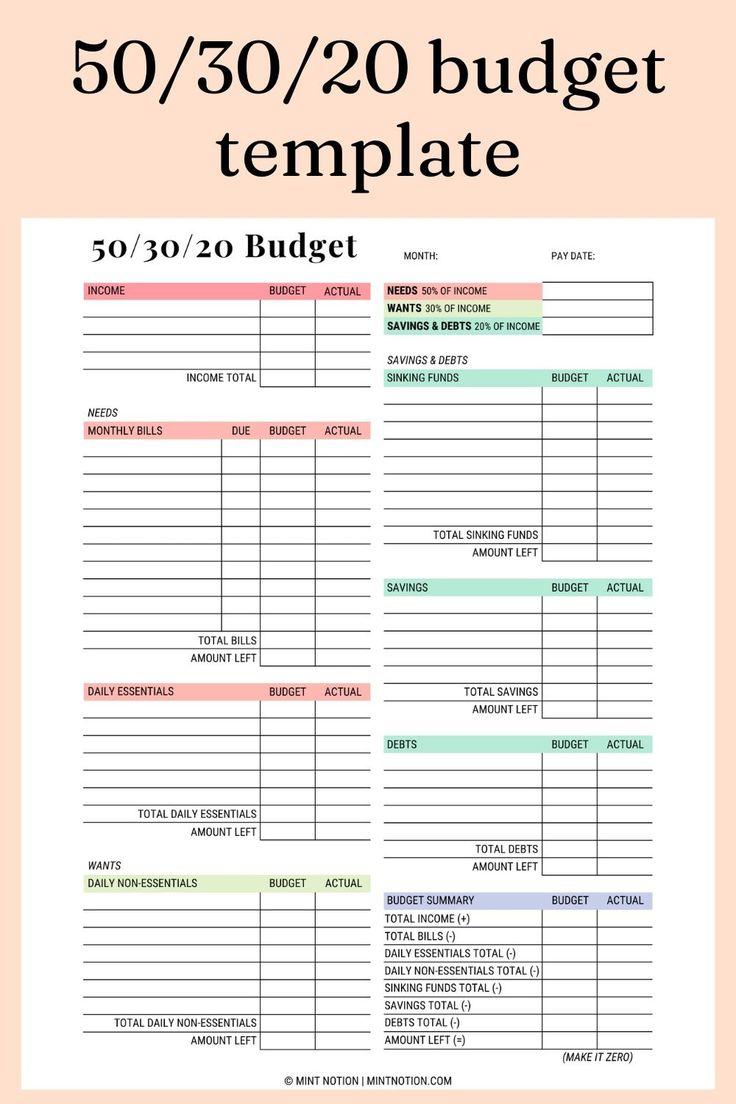

With a comprehensive overview of your expenses, it’s time to allocate funds strategically. Use the 50/30/20 rule as a guideline: allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. Consider using budgeting tools or apps to track your spending in real-time, ensuring you stay on course. Here are some tips to enhance your budgeting strategy:

- Automate savings: Set up automatic transfers to your savings account to ensure consistent growth.

- Review and adjust: Regularly assess your budget and make necessary adjustments to accommodate life changes.

- Involve the family: Encourage open discussions about finances to ensure everyone is on the same page.

- Prioritize debt repayment: Focus on clearing high-interest debts to free up more resources for your milestones.

By crafting a realistic budget, you’ll create a solid foundation for your family’s financial future, paving the way for achieving your dreams with confidence and clarity.

Investing Wisely to Secure Your Family’s Future

Achieving your family’s financial milestones requires a strategic approach that balances risk and growth. Diversification is key; spreading investments across different asset classes such as stocks, bonds, and real estate can help mitigate risk and maximize returns. Consider the following strategies to bolster your family’s financial security:

- Emergency Fund: Prioritize building a robust emergency fund to cover at least 3-6 months of living expenses, ensuring you have a safety net in unexpected situations.

- Retirement Accounts: Maximize contributions to retirement accounts like 401(k)s or IRAs. These accounts not only offer tax advantages but also provide long-term growth opportunities.

- Education Savings: If you have children, investing in education savings plans like 529 accounts can ease future tuition burdens, providing tax benefits and flexibility.

- Insurance: Safeguard your family’s financial future with adequate insurance coverage, including life, health, and disability insurance, to protect against unforeseen events.

By adopting these strategies, you can confidently navigate the financial landscape, ensuring that your family is well-prepared for both expected and unexpected life events. Remember, the cornerstone of wise investing is not just about growing wealth but also about securing peace of mind for your loved ones.

Regularly Reviewing and Adjusting Your Financial Plan

In the journey towards achieving your family’s financial goals, it’s essential to remain flexible and proactive. A financial plan is not a static document but a dynamic roadmap that requires regular evaluation and adjustment. Begin by setting a schedule to review your financial plan—consider quarterly check-ins to align with any changes in income, expenses, or life circumstances. During these reviews, ask yourself key questions: Have there been any significant changes in your financial situation? Are your investments performing as expected? Are there new financial goals to consider?

Engage your family in these discussions to ensure everyone is on the same page. Collaborative decision-making fosters accountability and collective motivation. Consider the following steps to fine-tune your plan:

- Analyze your budget: Look for areas where you can cut back or need to allocate more resources.

- Assess your risk tolerance: Life changes might affect your comfort with certain investment risks.

- Re-evaluate your goals: As your family grows, so might your financial aspirations.

- Update your estate plan: Ensure it reflects current wishes and legal requirements.

By consistently reviewing and adjusting your financial plan, you keep your family on track to meet its milestones, ensuring that your financial strategies evolve alongside your life’s journey.

{kind=link}